Lisa is an accomplished marketer with years of expertise in direct response marketing, digital marketing, data analytics and business development working with both B2C and B2B.

Shown above: Isa Medina’s Community Newsletter and previous month’s Newsletters. See more Community NewslettersHERE

Congratulations, Isa Medina you are the winner of this week’s $120 gift card!

Isa had the following words to say about her success after sending marketing from ProspectsPLUS!,

“I’ve been using ProspectPLUS! for over 8 years and it’s the best! I always get a listing using the campaigns. I would highly recommend agents create a campaign in a certain area and stick to it. The returns a priceless.” – Isa Medina

Thank you, Isa! Congratulations on your success!

NEW CONTEST STARTS NOW: Get the FIRST MONTH of Any Scheduled Campaign For FREE! ($120 value)

FARM, Call to Action Series Scheduled Campaign shown above.Learn more, HERE

Enter this week’s contest for a chance to win a $120 gift card covering the first month of ANY Scheduled Campaign.

The scheduled campaign includes 150 jumbo-sized postcards, sent standard postage (excluding data and tax. Includes only the first month free of a new campaign).

HOW TO ENTER: Just leave a review regarding how using marketing from ProspectsPLUS! has impacted your business, and you’re automatically entered into our next contest.

Mention a “scheduled campaign you’ve launched” in your review and your entry into the contest is doubled.

Launch a Scheduled Campaign today and save time on your marketing by automating it!

You Can Launch a Scheduled Campaign to any of the following Markets in Just Minutes:

Sphere of Influence Geographic Farm Just Sold Follow-up Holiday Renters Absentee Owners Expireds FSBOs Fence Sitters* Get More Listings* Empty Nesters* Move-Up Market*

(*Located under Farm Campaigns)

And, remember, YOU DON’T PAY for each mailing until it actually goes out (cancel or change each mailing up until the night before mailing goes out. The price shown at check out is per mailing, not campaign total).

TO GET STARTED:

STEP 1: Create your prospect list using our mailing list tools, HERE.

STEP 2: Then, once you have your list, choose your Campaign, select your start date, and add your list, HERE or hit “Launch a Scheduled Campaign”, below.

Digital marketing is hot with real estate agents. This provides an amazing opportunity for the agent who decides to take a different approach and become a BIG FISH in a small pond.

How do you do this? with direct mail.

Oh, I know what you’re thinking. “She works for a direct mail marketing company, of course, she will say this.”

Statistics, however, don’t lie. Direct mail marketing is not only strategic, but it can also be laser-focused to a particular audience and it works.

Why fish for listing leads in the huge ocean that is digital? Think about it; doesn’t it make more sense to cast your net in a smaller pond filled with people who you are certain ACTUALLY OWN HOMES?

Some things to consider

In a recent survey of real estate agents, 82% said their marketing goal this year is to “improve their social media presence,” according to Becky Brooks at theclose.com.

A worthy goal, but not very focused. Think about this: while they are chasing after Facebook leads, you’ll have little competition vying for attention in homeowners’ mailboxes.

With targeted direct mail you will not only reach homeowners. If you narrow your mailing list to only homeowners who have lived in their homes a certain number of years, or who live in starter homes or any other preferred criteria, you will have a far greater chance of taking listings than by randomly posting on social media.

For instance, by targeting homeowners who have been in their home for seven or more years, you’re creating a great list of potential fence-sitters to go after.

Fence Sitter postcard campaign shown above. To learn more, click HERE

Another thing to consider is the pandemic. In a recent USPS study, slightly more than 40% of Americans said that since the pandemic began, their excitement about receiving mail increased.

Nearly half of respondents said that a direct mail piece prompted them to go online to get more information about the sender.

The volume of direct mail plummeted from “… 213 billion pieces …” in 2016 to 120 billion last year. Interestingly, despite the drop in volume, the response rate skyrocketed nearly 200%.

You’ll have far less competition for eyes on your mail pieces and a better response rate than ever before.

Who makes up your potential seller audience?

Now that we’ve got you looking for listings in all the right places, what will you be sending? Keep in mind your audience – older generations, such as Baby Boomers and Gen X make up 75% of the real estate market combined.

When considering your direct mail marketing piece, don’t take valuable time out of your day to create marketing from scratch.

ProspectsPLUS! offers hundreds of marketing templates targeted specifically to your niche audience and designed by direct response experts.

Next, determine your recipient’s needs (boomers may want to downsize or move near their grown children) and offer a solution that is compelling (don’t worry ProspectsPLUS! has this covered for you as well). Check out the Empty Nest Series located under Farm campaigns.

Decide on the compelling offer to get those homeowners reaching out

A market update is always a good way to break the ice. Yes, it may be time-consuming, but it doesn’t have to be.

A simple chart of recently listeds, under contracts, and solds, along with bedrooms, baths, square footage, and prices, is something that hits my mailbox once a quarter. Do I read it?

You bet I do!

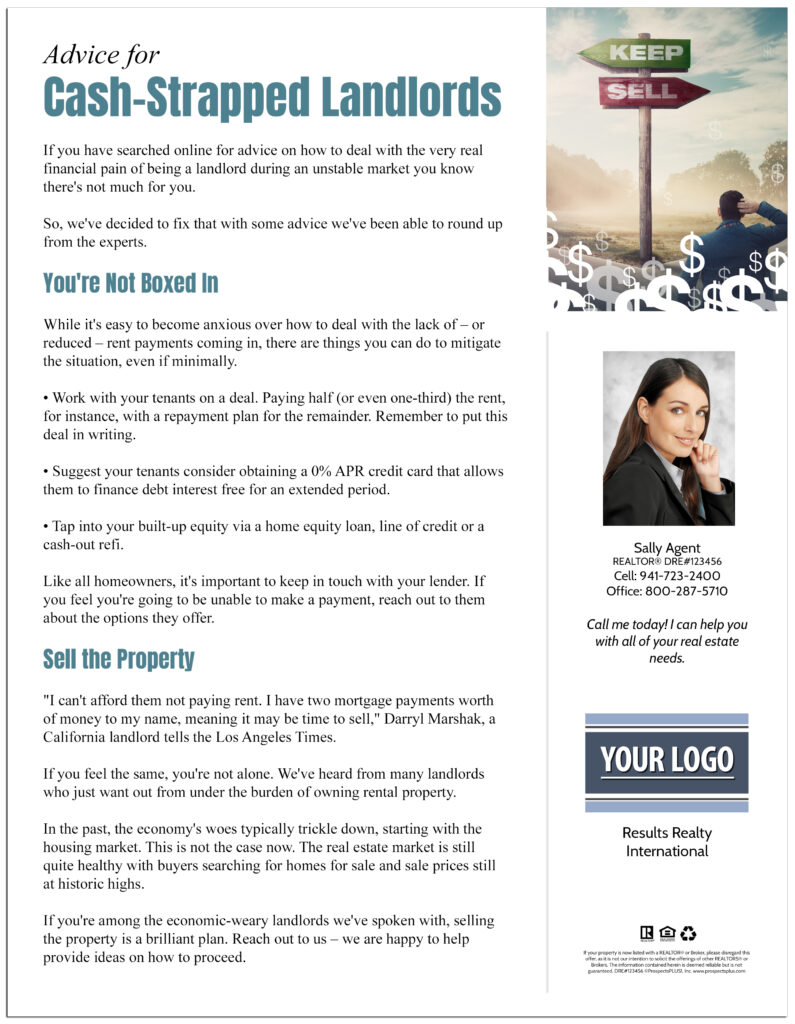

Then, there are the absentee owners to consider. Many have been hit hard by the rent moratorium and want out from under their investments. Take a look at what we offer to market to these possible listers.

If you have a freebie they can download or you can deliver, all the better. Offer them the Direct Response Report, Advice For Cash-Strapped Landlords.

Consistency is key in any lead generation campaign, so send just-listed and just-sold postcards when appropriate. Keep reminding them just how much their neighbors are getting for their homes in this on-fire sellers’ market.

FOMO (fear of missing out) is real.

Another way to keep those listings flowing? A YEAR ROUND Holiday Postcard Campaign.Staying top of mind with Your Sphere & Farm is easy with a Monthly Holiday Campaign.

And, Holiday Campaigns are ON SALE 10% OFF the first month– 3 More Days!

Holiday Postcard Campaign (shown above). Learn more, HERE

TO LAUNCH A HOLIDAY CAMPAIGN:

Hit the “CLICK HERE” link, below, to schedule your campaign (from a desktop or laptop computer).

USE PROMO CODE: HOLIDAY10 to get 10% Off at check out.

And, remember, YOU DON’T PAY for each mailing until it actually goes out (cancel or change up until the night before the mailing goes out). This sale expires 10/2/21.

Please reach out to our support team at 866.405.3638 with questions or if there is anything we can do to help you with your success.

PLUS: When you have time…below are some helpful tools to support your success.

1. The Free 12 Month Done-For-You Strategic Marketing Plan

The Real Estate Marketing Planner is a powerful 12-Month-Guide that strategically defines what marketing to do when. Four key market segments are included, Niche Marketing, Get More Listings, Geographic Farming, and Sphere of Influence. –Click Here

2. The Free Interactive Real Estate Business Plan

The Free Interactive Real Estate Business Plan allows you to enter your business goals for this year and get a breakdown of how many prospects, listings, closing, and so on are needed to reach your goals. – Click Here

3. The Automated Way to Become a Neighborhood Brand

Become branded in a specific neighborhood with a 12X15 marketing piece sent automatically each month to an exclusive carrier route. Watch this video to learn more or Click Here.

4. The Free Real Estate Mailing List Guide

The Real Estate Mailing List Guide outlines the top tools for generating targeted prospecting lists including Baby Boomers, Empty Nesters, Investors, Lifestyle Interests, High-Income Renters, Move-Up Markets, and more. The Guide also defines done-for-you marketing campaigns to match these markets. –Click Here

5. The Become a Listing Legend Free eBook

Ready to take a vertical leap in your real estate career? If you’re looking for inspiration…and the tools and methods to dominate a market and go to the top in real estate…you’ll find them in this free book. – Click Here

6. The Free Online ROI Calculator

Consistency and automation are the keys to success. Discover how effective direct mail marketing can dramatically increase your bottom line. Enter your statistics in our Free online ROI Calculator and click the ‘CALCULATE MY ROI’ button to see your results instantly! –Click Here

7. The Free Real Estate Marketing Guide “CRUSH IT”

The “Crush It” Guide includes easy steps to launching an effective direct mail marketing campaign, how to create a targeted prospect list, the perfect way to layout marketing materials for success, seven opportunities available to target in your area right now. –Click Here

Have you ever puzzled over what value you offer potential and existing clients that no other agent (or few others) offer?

Or, do you bundle up the same service as every other agent in town in the hope that it will be enough to prove to consumers why you deserve their business?

Determining your “unique value proposition,” or UVP for short, is critical, especially if you work in a market saturated with other real estate agents.

Quick explainer for newbies

A UVP “… is a concise, straight-to-the-point statement about the benefits you offer customers,” according to Solomon Thimothy at inc.com. “In other words, it’s an explanation of what makes you different,” he concludes.

It sets you apart from other agents. “It’s the promise you make to your customers and clients to deliver a unique experience, claims Tony Khuon at agilelifestyle.com.

So how do I come up with this UVP?

Think about what you can offer that few other agents do. If you’re a veteran, brush up on the VA home loan. Your UVP is that you are uniquely qualified to work with veterans.

If you’re an ace marketer or come from a marketing background you no doubt offer creative marketing solutions to home sellers. Solutions other agents can’t match. That’s an amazing UVP.

While many agents have started offering free services to their listing clients, the number still remains small. Stand out from the crowd by offering one or more of the following:

Free staging

Free housecleaning

Free curb appeal consultation

Free handyperson services (such as two hours of services, or something similar)

Yes, the thought of paying for these services is uncomfortable, but homeowners value these and, therefore, they make a dandy UVP.

Two more “services” that consumers find attractive are discounting your commission or giving a portion of your commission back to the community.

You don’t need to spend money, however, for what you offer to be considered valuable. “Homes I list sell for an average of 3% or more above list price.”

If true, that’s a pretty compelling UVP.

Remember to add your unique service to all of your marketing as a powerful call to action.

Your UVP needs to be simple, both in length and in word choice. Here’s an example of what not to do:

We are “… a dominant online presence with a combination of innovative marketing and strategic outreach. Cutting-edge lead capture and unique tracking URL’s ensure exposure and buyer retention.”

Put yourself in the shoes of a consumer reading this UVP on the group’s website.

What is “lead capture?” And “cutting edge” these terms have become absolute turn-offs. Tracking URL’s? Buyer retention? Where is the part of the UVP that allows the reader to clearly understand the value this team offers?

Then, ironically, this same UVP shows up on seven other real estate websites. Seven agents trying to prove what makes them different share a UVP with seven other brokerages.

Here’s another that we found. “Our astute team creates a plethora of assets unique to your home.”

Aside from dumping the words “astute” and “plethora,” this real estate team needs to describe exactly what “assets” they will “create.”

If you can save consumers money on their real estate deal, make the process easier or make it quicker, you’ve got yourself the makings of a UVP that will attract real estate clients.

Did you know our Holiday Scheduled Campaign is currently on sale 10% OFF the first month?

Farm, Holiday Scheduled Campaign is shown above. Learn more, HERE

TO LAUNCH A HOLIDAY CAMPAIGN:

Hit “CLICK HERE”, below (from a desktop or laptop computer).

USE PROMO CODE: HOLIDAY10 to get 10% Off at check out.

And, remember, YOU DON’T PAY for each mailing until it actually goes out (cancel or change each mailing up until the night before it goes out). This sale expires on 10/02/21.

Please reach out to our support team at 866.405.3638 with questions or if there is anything we can do to help you with your success.

PLUS: When you have time…below are some helpful tools to support your success.

1. The Free 12 Month Done-For-You Strategic Marketing Plan

The Real Estate Marketing Planner is a powerful 12-Month-Guide that strategically defines what marketing to do when. Four key market segments are included, Niche Marketing, Get More Listings, Geographic Farming, and Sphere of Influence. –Click Here

2. The Free Interactive Real Estate Business Plan

The Free Interactive Real Estate Business Plan allows you to enter your business goals for this year and get a breakdown of how many prospects, listings, closing, and so on are needed to reach your goals. – Click Here

3. The Automated Way to Become a Neighborhood Brand

Become branded in a specific neighborhood with a 12X15 marketing piece sent automatically each month to an exclusive carrier route. Watch this video to learn more or Click Here.

4. The Free Real Estate Mailing List Guide

The Real Estate Mailing List Guide outlines the top tools for generating targeted prospecting lists including Baby Boomers, Empty Nesters, Investors, Lifestyle Interests, High-Income Renters, Move-Up Markets, and more. The Guide also defines done-for-you marketing campaigns to match these markets. –Click Here

5. The Become a Listing Legend Free eBook

Ready to take a vertical leap in your real estate career? If you’re looking for inspiration…and the tools and methods to dominate a market and go to the top in real estate…you’ll find them in this free book. – Click Here

6. The Free Online ROI Calculator

Consistency and automation are the keys to success. Discover how effective direct mail marketing can dramatically increase your bottom line. Enter your statistics in our Free online ROI Calculator and click the ‘CALCULATE MY ROI’ button to see your results instantly! –Click Here

7. The Free Real Estate Marketing Guide “CRUSH IT”

The “Crush It” Guide includes easy steps to launching an effective direct mail marketing campaign, how to create a targeted prospect list, the perfect way to layout marketing materials for success, seven opportunities available to target in your area right now. –Click Here

Shown above: Postcards from various Just Sold Series and Donna Perri’s Just Sold postcard. See more Just Sold postcards HERE

Congratulations, Donna Perri you are the winner of this week’s $120 gift card!

Donna had the following words to say about her success after sending a Just Listed postcard through ProspectsPLUS!,

“I send these postcards to a 3-5 mi radius of each and every sale. They pay for themselves over and over. I have gotten five listings in six months from ProspectsPLUS!. I will continue using them in my marketing plan for sure. It makes farming easy and effective.” – Donna Perri

Thank you, Donna! You are a real estate rock star! Keep it up!

NEW CONTEST STARTS NOW: Get the FIRST MONTH of Any Scheduled Campaign For FREE! ($120 value)

FARM, Call to Action Series Scheduled Campaign shown above.Learn more, HERE

Enter this week’s contest for a chance to win a $120 gift card covering the first month of ANY Scheduled Campaign.

The scheduled campaign includes 150 jumbo-sized postcards, sent standard postage (excluding data and tax. Includes only the first month free of a new campaign).

HOW TO ENTER: Just leave a review regarding how using marketing from ProspectsPLUS! has impacted your business, and you’re automatically entered into our next contest.

Mention a “scheduled campaign you’ve launched” in your review and your entry into the contest is doubled.

Launch a Scheduled Campaign today and save time on your marketing by automating it!

You Can Launch a Scheduled Campaign to any of the following Markets in Just Minutes:

Sphere of Influence Geographic Farm Just Sold Follow-up Holiday Renters Absentee Owners Expireds FSBOs Fence Sitters* Get More Listings* Empty Nesters* Move-Up Market*

(*Located under Farm Campaigns)

And, remember, YOU DON’T PAY for each mailing until it actually goes out (cancel or change each mailing up until the night before mailing goes out. The price shown at check out is per mailing, not campaign total).

TO GET STARTED:

STEP 1: Create your prospect list using our mailing list tools, HERE.

STEP 2: Then, once you have your list, choose your Campaign, select your start date, and add your list, HERE or hit “Launch a Scheduled Campaign”, below.